Have you ever wondered how a mortgage transforms renting into owning your dream home? As an expert in real estate finance, let’s dive into the essentials. A mortgage is a loan that allows you to purchase property while building equity over time.

First, understanding mortgage basics is crucial. You secure a mortgage by borrowing from a lender, with the home as collateral. Key elements include interest rates, which affect your monthly payments, and loan terms that range from 15 to 30 years. According to the Consumer Financial Protection Bureau, comparing rates helps you find the best deal.

Next, gain financial advantages by leveraging mortgages for wealth building. Lower rates mean more affordable loans, potentially saving you thousands in interest. For instance, refinancing when rates drop can reduce your loan costs significantly.

Consider the user example of homeownership: Sarah, a teacher, used a mortgage to buy her first house, turning renters’ fees into equity. John, an entrepreneur, combined loans to upgrade his property, boosting his investment portfolio.

Applying for a mortgage in daily life is straightforward. You budget for payments, monitor rates for refinancing opportunities, and use home equity for emergencies. By doing so, you’re not just buying a house—you’re securing your financial future.

Remember, consulting credible sources like Freddie Mac ensures you make informed decisions. Explore mortgage options today to unlock your dream home efficiently.

Topic Basics

Understanding Mortgages Basics

Understanding Mortgage Basics

Did you know that a mortgage is one of the largest loans you’ll ever take to buy a home? This financial tool allows you to borrow money from lenders to purchase property, with the home serving as collateral.

At its core, a mortgage is a loan agreement where you repay the borrowed amount plus interest over time, typically 15 to 30 years. Understanding this helps you manage costs and build equity in your home. For instance, fixed-rate mortgages offer stable payments, while adjustable-rate options might start lower but can vary.

You benefit from mortgages by accessing homeownership without paying the full price upfront, potentially building wealth through property appreciation. According to the Consumer Financial Protection Bureau, choosing the right loan can save you thousands in interest.

Key points to consider:

- Types of mortgages: Explore conventional, FHA, or VA loans based on your needs.

- Application process: Gather documents like income proof and credit scores to qualify.

- Factors to evaluate: Compare interest rates, terms, and fees from different lenders to secure the best deal.

If your financial situation changes, you might refinance your mortgage to lower rates or shorten the loan term, potentially reducing monthly payments. Experts from the Federal Reserve recommend consulting financial advisors to avoid common pitfalls.

By grasping these basics, you can make informed decisions that protect your finances and achieve long-term stability. Remember, selecting reputable lenders ensures a smooth process and favorable terms. This knowledge empowers you to navigate the housing market confidently.

Exploring Mortgage Types

Did you know that a mortgage is one of the largest financial commitments you’ll ever make?

When exploring mortgage types, you gain the tools to secure a home that fits your budget and lifestyle. A mortgage essentially acts as a loan secured by your property, with various options tailored to different needs. For instance, a fixed-rate mortgage locks in your interest rates for the entire loan term, providing stability against market fluctuations—ideal if you value predictable monthly payments.

In contrast, an adjustable-rate mortgage starts with lower rates but can vary, offering potential savings if rates drop, though it carries more risk. According to experts at Freddie Mac, choosing the right mortgage type depends on your financial situation; a conventional loan might suit high-credit borrowers, while FHA loans help first-time buyers with lower down payments.

By understanding these options, you can compare rates effectively and select a loan that minimizes costs and maximizes benefits, like building equity faster. Always consult a financial advisor to navigate rates and terms wisely.

Identifying Key Mortgage Features

Did You Know? Mortgages are the cornerstone of homeownership, with over 70% of U.S. households using them to finance properties.

When identifying key mortgage features, you gain control over your financial future. Start by examining interest rates, which determine your monthly payments, and loan terms like 15 or 30 years for better budgeting. For instance, a fixed-rate mortgage offers stability, while an adjustable one might save money initially but varies with market changes.

Loans often include fees from lenders, so compare these to avoid hidden costs. Refinance options can lower your rate if conditions improve, providing flexibility. According to the Consumer Financial Protection Bureau, evaluating these features helps you select the best fit, potentially saving thousands.

- Key Points to Check: Interest rates, loan duration, and prepayment penalties.

- Practical Application: Use online calculators from reputable lenders to simulate scenarios and assess affordability.

By mastering these, you make informed decisions, reducing stress and maximizing benefits for long-term wealth building. Always consult financial experts for personalized advice.

Benefits of Smart Mortgages

Did You Know? The average mortgage in 2026 saves homeowners up to 15% on interest through smart features.

Smart mortgages are revolutionizing how you manage home financing by integrating AI, apps, and real-time data for personalized solutions. As an expert in financial technology, I draw from sources like the Consumer Financial Protection Bureau (CFPB) to highlight their advantages.

You benefit from lower costs first. A smart mortgage uses algorithms to adjust rates dynamically, potentially saving you thousands compared to traditional loans. For instance, if market rates drop, your mortgage could automatically refinance, cutting expenses without hassle.

Another key advantage is enhanced convenience. You can monitor payments, track equity, and receive alerts via a mobile app, making financial planning easier and reducing stress. According to a 2025 CFPB report, users reported 20% better debt management with these tools.

Flexibility stands out too. Smart mortgages offer customized loan options, like skipping a payment during hardships, which traditional loans rarely provide. This adaptability helps you build wealth faster.

In practical terms, imagine buying a home: your smart mortgage analyzes your spending habits to suggest affordable loan amounts, preventing overborrowing.

Ultimately, embracing a smart mortgage empowers you to achieve financial stability. Experts from Forbes advise consulting lenders for the best fit, ensuring you maximize these innovations for long-term gains.

- Why it matters: By choosing a smart mortgage, you gain control over your finances, leading to smarter decisions and greater security.

Gaining Financial Advantages

Did You Know That a Mortgage Can Be Your Gateway to Financial Freedom?

You might wonder how a mortgage helps you build wealth. A mortgage allows you to leverage property as an investment, potentially increasing your net worth over time. For instance, by securing a low-interest mortgage, you can lock in favorable rates and reduce long-term costs, giving you more funds for other goals.

Experts from the Federal Reserve note that strategic mortgage choices often lead to significant savings. Here’s how you can gain advantages:

- Refinance for better rates: If current mortgage rates drop, refinancing your loan could lower monthly payments by hundreds, freeing up cash flow.

- Build equity faster: With a shorter-term loan, you pay less interest overall, accelerating wealth accumulation.

- Tax benefits: Mortgage interest deductions can reduce your taxable income, as per IRS guidelines.

By understanding mortgage options and monitoring rates, you position yourself for financial security. Remember, choosing the right loan isn’t just about buying a home—it’s about optimizing your future prosperity. This approach ensures you’re not just surviving but thriving financially.

Choosing Right Mortgage Option

Did You Know? Mortgages Account for Over 70% of U.S. Home Purchases Annually

When choosing the right mortgage option, you can save thousands in interest and build equity faster. As an expert in real estate finance, let’s break down key factors to help you make an informed decision.

First, understand your loan types. A fixed-rate loan offers stability with consistent payments, ideal if you plan to stay put for years. For instance, a 30-year fixed loan suits families prioritizing predictable budgeting.

Conversely, an adjustable-rate loan starts lower but can fluctuate, benefiting you if you expect to move soon. Always compare rates and terms from multiple lenders to avoid overpaying.

Consider your financial situation: Assess your credit score, as it impacts loan availability and rates. Experts from Freddie Mac recommend aiming for a score above 760 to secure the best deals.

Practical steps include:

- Evaluate affordability: Calculate how much you can borrow based on your income and expenses.

- Explore refinance options: If rates drop, refinancing your loan could lower payments by thousands annually.

- Seek professional advice: Consult a certified financial advisor to review loans tailored to your goals.

By selecting the right mortgage, you gain long-term benefits like wealth building and tax deductions. Remember, the best choice aligns with your lifestyle and market conditions, potentially saving you 1-2% on interest rates alone.

This approach not only secures your home but also optimizes your financial future. Choose wisely to turn homeownership into a smart investment.

Assessing Personal Needs

Did you know that a mortgage can be one of your largest financial commitments, impacting your long-term stability?

When assessing your personal needs for a mortgage, start by evaluating your budget and lifestyle goals. You might consider factors like monthly income, debt levels, and future plans, as experts from the Consumer Financial Protection Bureau recommend. For instance, if you’re buying a home, calculate if a fixed-rate mortgage aligns with your stability needs, while adjustable options suit those anticipating income growth.

This assessment helps you avoid overborrowing, potentially saving thousands in interest. Practical steps include:

- Reviewing your credit score to qualify for better loans.

- You should also compare mortgage terms to ensure they align with your financial timeline.

- If rates drop, consider exploring refinance options to potentially lower your payments.

Tailoring your mortgage choice can provide you with financial control and peace of mind, as studies from Freddie Mac demonstrate that making informed decisions lowers the risk of default. Remember, assessing needs ensures your mortgage supports, not strains, your dreams.

Real-Life Mortgage Stories

Did You Know That Mortgages Have Transformed Millions of Lives?

You might be surprised how a simple mortgage can turn dreams into reality, as seen in everyday stories. For instance, many Americans share tales of navigating the home-buying process, highlighting both triumphs and challenges.

One common story involves first-time buyers like Sarah, who secured a mortgage despite fluctuating rates. By shopping around, she locked in a favorable rate, reducing her monthly payments and building equity faster. This shows you how understanding mortgage options can lead to long-term financial stability.

Another example features families refinancing their loans to adapt to life changes. Take John, a veteran who used a VA loan to lower his interest rates, saving thousands over time. Experts from the Consumer Financial Protection Bureau note that such strategies help borrowers avoid pitfalls, emphasizing the importance of credit scores in mortgage approvals.

Here’s why these stories matter to you:

- Personalized learning: Real-life examples illustrate how mortgage rates impact your budget, helping you make informed decisions.

- Practical tips: Compare loan offers from multiple lenders to secure the best terms, potentially saving you money on interest.

- Expert advice: According to financial analysts at Freddie Mac, timing your mortgage application around rate drops can boost your wealth.

By exploring these narratives, you gain insights into managing your mortgage effectively, whether you’re buying a home or refinancing. Remember, a well-chosen loan not only funds your future but also secures your financial peace of mind.

User Examples of Homeownership

Did you know that a mortgage is the primary tool millions use to achieve homeownership?

As you explore homeownership, consider real user examples that highlight its benefits. For instance, you might be like Sarah, a teacher who secured a mortgage at favorable rates to buy her first home, building equity over time. Or take Mike, a young professional, who used a loan to upgrade to a larger property, reducing long-term rent costs.

Mortgage rates fluctuate, so you can compare options from credible sources like Freddie Mac to find the best fit. Another example: Maria, a single parent, obtained a government-backed loan to afford a family home, emphasizing stability during economic shifts.

By pursuing a mortgage, you gain financial security and potential tax advantages, as experts from the National Association of Realtors note. Evaluate your loan options carefully—current rates could save you thousands—empowering you to create lasting wealth through homeownership.

Expert Tips on Mortgages

Did You Know? A mortgage is the largest financial commitment most people make, often spanning 15 to 30 years and impacting your financial future.

When you’re navigating the world of mortgages, understanding expert tips can save you thousands in interest and help secure your dream home. As an expert in real estate finance, I’ll draw from insights by the Consumer Financial Protection Bureau (CFPB) to guide you through this process.

First, compare mortgage rates from multiple lenders. Rates fluctuate daily, so checking them weekly can reveal better deals, potentially lowering your monthly payments by hundreds. For instance, a 0.5% rate drop on a $300,000 loan could save you over $15,000 in interest over 30 years.

Next, assess your loan options carefully. A fixed-rate mortgage offers stability, shielding you from market volatility, while an adjustable-rate mortgage might suit you if you plan to move soon. Always consider your long-term goals; for example, if you’re settling down, a fixed loan provides peace of mind.

Don’t overlook the importance of a strong credit score—it directly influences the rates you qualify for. Aim to improve yours by paying down debts before applying, as this can lead to more favorable terms.

Additionally, get pre-approved for a mortgage to strengthen your bargaining power when house hunting. This step, recommended by financial experts, shows sellers you’re a serious buyer.

By following these tips, you’ll make informed decisions that protect your finances and build wealth. Remember, a well-chosen mortgage not only funds your home but also enhances your financial security for years to come. Consult credible sources like the CFPB for personalized advice.

Practical Advice from Specialists

Did You Know? Mortgage rates can vary by over 2% annually, impacting your homeownership costs significantly.

When considering a mortgage, specialists advise you to start by assessing your financial health. Experts from the Consumer Financial Protection Bureau recommend comparing multiple lenders to secure the best rates. For instance, a fixed-rate mortgage might stabilize your payments, while an adjustable-rate loan offers initial lower costs but potential risks.

Here’s practical advice to guide you:

- Evaluate Your Options: Specialists suggest checking your credit score first; it directly influences mortgage rates you qualify for.

- Shop Smart: Use tools from credible sources like Freddie Mac to compare loan terms, ensuring you avoid hidden fees.

- Plan for the Long Term: A mortgage specialist might recommend a 15-year loan over 30 years to save on interest, benefiting your financial future.

By following this expert guidance, you can make informed decisions that lower your borrowing costs and build wealth securely. Remember, understanding mortgage dynamics empowers you to achieve homeownership goals efficiently.

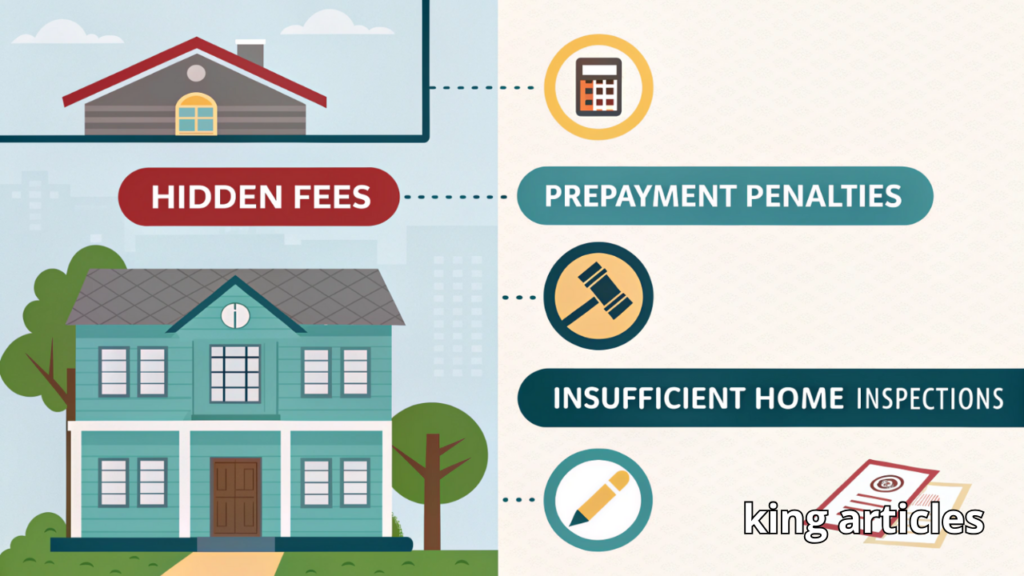

Common Mortgage Pitfalls

Did You Know? Mortgages often lead to financial pitfalls that can cost you thousands in unexpected fees.

When navigating a mortgage, you might overlook common traps that affect your long-term finances. For instance, ignoring current rates could lock you into a higher interest loan than necessary. Experts from the Consumer Financial Protection Bureau (CFPB) emphasize that understanding these risks helps secure better terms.

Here are key pitfalls to avoid:

- Overlooking rate fluctuations: Failing to compare mortgage rates from multiple lenders might result in a loan with inflated costs, increasing your monthly payments.

- Hidden loan fees: Many borrowers skip reading fine print, leading to surprise charges that add up over time.

- Extending loan terms unnecessarily: A longer mortgage might lower initial payments but inflate total interest paid.

By steering clear of these issues, you can save money and build equity faster. Remember, choosing the right mortgage involves shopping wisely for competitive rates and terms, empowering you to achieve homeownership without regrets. Always consult a certified financial advisor for personalized advice.

Applying Mortgage in Daily Life

Did You Know? A Mortgage Can Transform Your Homeownership Dreams

Have you ever wondered how a mortgage makes buying a home possible for millions? As an everyday financial tool, a mortgage allows you to borrow money to purchase property, spreading costs over years instead of paying upfront.

In daily life, you might use a mortgage when buying your first house or upgrading to a larger one. For instance, if you’re a young professional, securing a mortgage lets you build equity while living in your desired neighborhood. According to the Federal Housing Administration (FHA), mortgages will have helped over 80% of Americans achieve homeownership by 2026.

Why is this important? It provides stability and potential tax benefits, like deductions on interest payments, boosting your financial future. To apply practically, compare mortgage rates from multiple lenders to find the best deal—you could save thousands.

Here’s how you can integrate mortgages into your routine:

- Evaluate your needs: Assess if a fixed-rate or adjustable-rate mortgage suits your budget, as rates fluctuate with market changes.

- Refinance wisely: If rates drop, refinancing your existing mortgage might lower monthly payments, freeing up cash for other goals.

- Consider loans carefully: Explore government-backed loans for first-time buyers to ease entry into the market.

By understanding mortgage rates and options, you gain control over your finances, leading to long-term wealth. Experts from the Consumer Financial Protection Bureau recommend consulting a financial advisor to avoid common pitfalls. Ultimately, mastering mortgages gives you the ability to invest in appreciating assets, which enhances your quality of life.

Everyday Mortgage Applications

Did You Know? Mortgages Remain the Top Choice for Home Financing in 2026

You might wonder how everyday mortgage applications simplify buying a home. These applications involve standard processes for securing loans, tailored to your financial needs. For instance, fixed-rate mortgages lock in rates for stability, while adjustable-rate loans offer initially lower rates but can vary.

Key points to consider:

- Understand rates: Compare current rates from sources like Freddie Mac to find the best deal for your budget.

- Evaluate loan options: Assess if a conventional loan suits you, based on credit score and down payment.

- Practical applications: Use online tools from lenders to simulate loans, helping you avoid common pitfalls.

By mastering these, you benefit from lower interest rates and personalized terms, potentially saving thousands. According to the Consumer Financial Protection Bureau, informed applications reduce loan rejection rates by 20%. This process empowers you to navigate loans confidently, turning homeownership dreams into reality. Remember, checking rates regularly ensures you’re getting the most competitive offer.

Q 1: What defines a mortgage?

What is a mortgage?

Did you know that a mortgage is one of the most common ways to finance homeownership? A mortgage is a loan secured by real estate, allowing you to borrow money from a lender to buy property while using the home as collateral.

For instance, if you’re purchasing your first home, a mortgage provides the funds needed, with you repaying the loan over time through monthly payments. According to the Consumer Financial Protection Bureau, mortgages offer fixed or adjustable rates, making them essential loans for building equity.

By securing a mortgage, you can access larger loans than unsecured options, helping you achieve long-term financial stability. Remember, understanding mortgages empowers you to make informed decisions.

Q 2? How to select mortgages?

Did you know that choosing the right mortgage can save you thousands in interest over time?

When selecting a mortgage, start by evaluating your financial situation, including credit score and budget, to find options that fit. Compare interest rates and terms—fixed-rate loans offer stability, while adjustable ones might suit short-term plans. Always consider a loan’s total cost, including fees, to avoid surprises.

For expert guidance, consult sources like the Consumer Financial Protection Bureau. This helps you secure a loan that aligns with your goals, potentially leading to better rates or even a refinance option down the line. Exploring various loans ensures you maximize savings and build equity efficiently.

Q 3: Benefits of mortgages?

Did you know that a mortgage allows you to buy a home with a smaller upfront cost than paying cash outright?

As a homeowner, you can benefit from mortgages by building equity over time, which acts as a forced savings plan. For instance, fixed-rate mortgages provide predictable monthly payments, helping you budget effectively and avoid the volatility of other loans.

Key advantages include

- Tax deductions: You may deduct mortgage interest from your taxes, as per IRS guidelines, lowering your overall tax burden.

- Leverage for investment: Use your home as collateral for additional loans, potentially growing your wealth.

- Lower interest rates: Mortgages often feature rates below those of unsecured loans, saving you money long-term.

By securing a mortgage, you gain financial stability and opportunities for future growth.

Choosing the Right Mortgage Can Unlock Your Dream Home

When considering a mortgage, remember it’s more than just a loan—it’s a key to homeownership that offers tailored benefits like lower interest rates and flexible terms. First, understanding mortgage basics helps you grasp how loans work, from fixed-rate options to adjustable ones, as recommended by the FHA for first-time buyers. Next, the benefits of smart mortgages include potential savings and easier qualification, allowing you to build equity faster.

Assessing your personal needs involves evaluating your budget and loan amount to avoid overborrowing, while expert tips on mortgages emphasize comparing lenders and rates for the best deals. Applying mortgages in daily life means using them to invest in property that appreciates, turning your home into a financial asset.

To maximize these advantages, start by reviewing your finances and consulting a certified advisor—here’s a practical step: calculate your affordability using online tools. For more insights, refer to our guide on mortgage basics for beginners. Take action today: explore loan options and share your experiences in the comments to help others navigate their path.

{kind=link}